: 348

: 348

BUSN20016 RESEARCH IN BUSINESS, T1, 2019

ASSESSMENT 3

PROJECT TITLE: Impact of Operating Expenses on Income

Statements of Commonwealth Bank of Australia (CBA)

ASSESSMENT SHEET

|

Criteria |

Total marks |

Marks obtained |

Overall comments |

|

A detailed statement of the problem, research

aim, objectives and research questions |

10 |

|

|

|

A detailed justification and potential output

of the research |

10 |

|

|

|

The conceptual framework |

10 |

|

|

|

Methodology, organisation of the study,

project budget and schedule |

10 |

|

|

|

Accurate referencing, use of correct English

and logical sequences betweensentences and

paragraphs and a good introduction |

10 |

|

|

|

Total

= |

50 |

|

|

|

Mark reduction for Turnitin similarity (It's

up to the markers and unit coordinator's judgement) |

|

|

|

|

Mark reduction for late submission(5%

mark reduction for each day of late submission) |

|

|

|

|

Grand

Total= |

50 |

|

|

|

Key to grading and corresponding marking

scale: HD (42.5 and above out of 50 marks): Student demonstrates

outstanding understanding and interpretation of all aspects of the criteria. D (37.25 to 42.24 out of 50 marks): Student demonstrates

excellence in understanding and interpretation of almost all aspects of the

criteria with some minor corrections or additions needed. C (32.25 to 37.24 marks out of 50 marks): Student demonstrates very

good understanding and interpretation of most aspects of the criteria with

some need for additional work, additions or improvement. P (24.75 to 32.24 marks out of 50 marks): Student demonstrates good

understanding and interpretation of the criteria to warrant the award of a

Pass but requires considerable additional work, additions or improvement. F (below 24.7 marks out of 50 marks): Student demonstrates an

unsatisfactory understanding and interpretation of the criteria and requires

major additional work, additions or improvement to achieve a passing grade. |

|||

June 2019

Table of Contents

Justification for Research Project

Research Approach and Data Source

Data Collection Method and Technique

of Data Analysis

Budget and Scheduling and

Justification

Appendix 1:

Operating Expenses of CBA in 2016

Appendix 2:

Household Debt (% of GDP)

Appendix 3: Five

Year Financial Report of CBA (from 2015 to 2019)

Introduction

Financial performance of a business is liable to

portray the ability of the company to compete in the global market while

indicating potential growth opportunities. In this regard, focus on managing

operating expenses hold significant impact in supporting financial performance.

As opined by Tran (2015),

attempt of business entities to manage costs of operating activities can

present opportunity to regulate and control functional operations. It is also

crucial to manage business relations in terms of monitoring manufacturing and

production policies along with relationships with stakeholders. Moreover, focus

on controlling and allocating resources, including financial and human

resources are crucial to manage operating costs for supporting financial

improvement.

In the case of Australian banks, changing dynamics of

business policies and contemporary competitive market have facilitated chances

to focus on managing operations and related costs for further growth. For

instance, monetary policies are essential to attract the attention of the

customers for investing in Australian banks. This initiative due to

effectiveness of monetary policies can eventually lead to increased

profitability of respective banks (Borio, Gambacorta & Hofmann, 2017).

Besides, investments of bank in controlling taxable income and operating costs

including expenses for consulting services, employee remuneration, adoption of

technology and related legal fees can support a bank to improve profit margin.

In the opinion of Buckley, Weber & Dowell-Jones

(2015), the banking industry is devoted to deliver effective financial services

to a wide range of customers and hence insurance costs, directors fees, costs

of fixed assets and payroll are important factors to regulate operating

expenses. Regarding these aspects, emphasis on understanding the impact of

operating expenses of Commonwealth Bank of Australia (CBA) on

income statement of this bank can be effective to comment on financial

performance of Australian banks. It can also be influential in determining the

effectiveness of functional operations and related expenses for reflecting on

profit margin and ensure holistic growth of business.

Problem

Statement

Rapid changes in business dynamics

are accountable for restructuring financial performance of Australian banks in

terms of influencing profitability. According to Jin, Shan & Taylor (2015), increase in

operating expenses is liable to lower profit margin by allowing a business

entity to invest more in functional activities. However, influence of operating

expenses in controlling profit margin or income statement of a company can be

measured through evaluating net profit after tax (NPAT) of respective company.

In the context of Commonwealth Bank of Australia (CBA), increase in operating

expenses has been a significant issue for this company as it has affected

financial stability. As per statistical reports operating expense of the

company mentioned above increased up to 10,429 $m in 2016 from 9,993$m

in the previous year (Commbank.com.au, 2016). [Refer to Appendix 1]

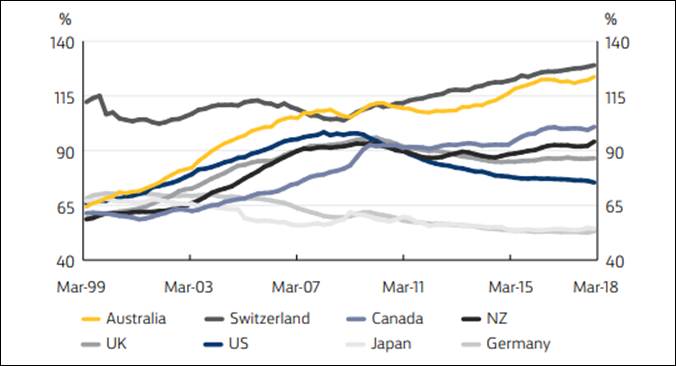

In addition, potential risks related

to shift to macro-economy and risks related to household debt have affected the

financial performance of banking industry of Australia. As per statistical

information, household debt increased up to 127% of GDP that

influences income statement of Australian banks (Commbank.com.au, 2019).

Moreover, changes in operating costs in terms of supporting the introduction of

new technologies and managing increased number of customers are also effective

to regulate income statement of banks (Alam, Alam & Hoque, 2019). In this

context, the inability of CBA to manage records of 20 million customers and

losing data of past 15 years raised a question on effectiveness of functional

activities (Bbc.com, 2018). Hence, improvement in technology to protect

confidential information of consumers is a crucial factor that can influence

operating expenses. [Refer to Appendix 2]

Along with this, potential threats

of money laundering and terrorist financing have also instigated chances for

banking industries to improve legal approaches and strengthen security systems

for ensuring financial growth (Daley & Wood, 2016). Attempt of banks to

protect confidential data of consumers and track records of financial transactions

is liable to reduce instances of breach in law. However, negligence and

inadequate security systems of banks including CBA has forced financial loss

(James, Sawyer & Wallschutzky, 2015). For

instance, CBA has to pay $700 million for being accused of

breaching anti money laundering regulations (Doran & Janda, 2018).

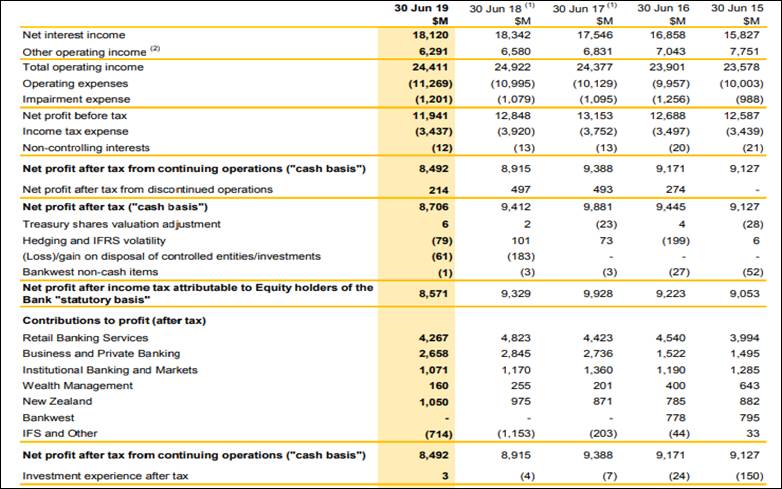

Moreover, business expansion and the increased number of customers have

resulted in rise in operating expenses. The operating expenses of CBA increased

up to 11,269$m in 2019 (Commbank.com.au, 2019). [Refer to Appendix 3]

Apart from this, adequacy of a bank to manage its

operating costs projects the efficiency of the organisation to manage resources

and operate functional activities (Ogilvy & Vail, 2018). It is also

effective to comment on financial performance in terms of inspecting profit

margin. Besides, operating cost can determine financial performance through

managing net profit after tax that reflects in the income statement of a

company. In case of CBA, net profit after tax has decreased to 8,492$m

in 2019 from 8,915$m in 2018 (Commbank.com.au, 2019). Furthermore, the

inability of this bank to check 778,370 accounts properly and

reluctance to check 53,506 reports related to transactions of more than

$10,000 using the IDMs (intelligent deposit machines)

have presented challenges for this company to encounter financial loss (Doran

& Janda, 2018). [Refer to Appendix 3]

Hence, focus on evaluating the influence of operating

costs on income statement of CBA by calculating net profit after

tax (NPAT) can enable chances to measure financial growth of this bank. It is

also significant in understanding effectiveness of resource allocation and

utilise technological advancements for improving operational activities (Bodle,

Cybinski Patti & Reza, 2016). Moreover, focus on

assessment of operating expenses can also present chances to identify potential

areas of further growth while following legal instructions. Besides, it can be

advantageous to maintain the standards of accounting for regulating operational

activities and ensuring improvement in financial performance (Ahmed &

Ndayisaba, 2016).

Aim,

Objectives and Scope

The prime aim of this research would

be to explore the implication of operating expenses on the income statement in

regard to functional activities and financial performance of the CBA

(Commonwealth Bank of Australia).

The main objectives of this study

can be listed as below-

● To evaluate the influence of financial performance in

holistic business growth of CBA

● To identify factors that can be effective to control

operating expenses of CBA

● To identify how operating expenses of CBA influences

income statements

● To formulate effective suggestions for controlling

operating costs and supporting the financial growth of CBA

Attempt to examine the influence of

operating costs on the income statement of the bank mentioned above would be

effective to comment on effectiveness of resource allocation capability of the

bank. Moreover, it would support to evaluate financial performance of the bank

by assessing income statements and commenting on net profit after tax (NPAT),

gross

profit and annual revenue (Ongayi et al. 2018). This can also support to

understand potential aspects of financial growth of this company while

calculating profit ratio. Besides, it would deliver chances to identify major

factors that influence financial performance of the bank and evaluate

relationships with stakeholders to promote business growth. Along with these,

operating costs can also help to measure return on investment (ROI) and express

payment system (EPS) for evaluating technological and legal aspects to

influence profitability of the aforementioned Australian bank (Laing &

Dunbar, 2015).

Justification

for Research Project

This research would focus on

identifying implications of operating costs on income statement of CBA to

understand the effectiveness of the bank for controlling resources. It would

also help to locate functional efficacy and the financial performance of the

bank. Moreover, operating expenses being a parameter to measure initiatives of

the bank to regulate functional activities can help to assess business strategy

of the company (Tang, Chen & Lin, 2016). Besides, it can support to assess

financial market of Australia in terms of evaluating growth prospects of

financial service providers including CBA. Moreover, the research would be

beneficial to focus on utilisation of fixed assets and funds for reducing

operating expenses and generating maximum profit for ensuring business growth

(Yen, Sarath & Ahmed, 2016).

Apart from this, analysis of the

impact of operating expenses on the income statement would also help to comment

on accounting standards (Wines & Scarborough, 2015). It would generate

opportunity to comment on tax implications while tracking changes in profit

margin and calculating net profit after tax (NPAT) of the

CBA. In addition, emphasis on identifying factors that have affected operating

costs can extend chances to modify process of financial and human resource

allocation (Yapa, Kraal & Joshi, 2015). It can also allow Australian banks

to focus on improving corporate image in terms of maintaining international

financial standards. Furthermore, the research would contribute to develop an

understanding of cash flow stability and tax implications while measuring

social and legal aspects for supporting gradual improvement in financial

performance (Joubert, Garvie & Parle, 2017).

Potential

Outputs

The research intends to comment on

financial performance of Australian banks in terms of measuring influence of

operational expenses on income statement of CBA. Successful completion of this

research would be effective to understand efficacy of operations management

department of CBA to allocate resources. It would also support to identify

factors including remuneration of employees, insurance costs, maintenance of

fixed assets, and adoption of technology and tax implications to reflect on

financial performance (Xu, Davidson & Cheong, 2017). Moreover, the research

would contribute to explore the perspective of financial resource management by

assessing investment in operating expenses. This can ultimately support in

assessment of financial statements for calculating return on investments (ROI) and

gross

profit (Wong & Joshi, 2015).

In addition, it would help to

determine the influence of the factors to increase or decrease operating costs

that ultimately impacts on financial performance of an organisation. Besides,

implications of operating expenses to control financial performance or net

profit margin would also be explored in this research. It can explain the

relationship between operating expenses and profit margin by calculating net

profit after tax (NPAT) (Taplin et al. 2019).

It would also help to measure effectiveness of functional operations of

financial service providers including CBA. Along with this, the research can

contribute to understand required costs and changes in financial performance

due to compliance with accounting standards and legal guidelines while adopting

advanced technology to improve holistic performance (Zeller, Kostolansky & Bozoudis, 2019).

Conceptual

Framework

Figure

1: Conceptual Framework

(Source: Developed from Borio, Gambacorta &

Hofmann, 2017)

Research

Hypothesis

H0: Operational expenses

do not hold statistically significant impact on net profit after tax (NPAT) for

regulating income statement of Commonwealth Bank of Australia (CBA).

H1: Operational expenses

hold statistically significant impact on net profit after tax (NPAT) for

regulating income statement of Commonwealth Bank of Australia (CBA).

Methodology

Identifying a particular method of

research allows opportunity to conduct a systematic and scientific study for

meeting research aim and objectives (Bell, Bryman & Harley, 2018). This particular research

project would follow a secondary method of research to

collect relevant information on the influence of operating expenses on revenue

and NPAT (net profit after tax). Moreover, descriptive research approach would

be applied while adopting a quantitative research method to identify the

influence of operating expenses on the income statement of CBA.

Research

Approach and Data Source

This study would follow a secondary

method of research while applying positivism philosophy, descriptive design and

deductive approach. According to Kumar (2019), selection of positivism philosophy allows

opportunity to collect quantifiable and observable data to obtain reliable

research outcomes. In this particular case, incorporation of positivism

philosophy would be essential to interpret raw data into meaningful

information. Moreover, descriptive design can support to describe patterns in

obtained data sets and comment on variables that influence operating costs (Flick, 2015). Deductive

approach, on the other hand, would help to test the research hypothesis based

on existing theories. It would also be advantageous to develop a research

strategy for interpreting obtained secondary data and address research

hypothesis while establishing causal relationship between research variables (Walliman, 2017).

Apart from these, the research would

apply a secondary method of research to collect required information

from secondary sources including books, scholarly journals, websites, newspaper

articles and company reports (Bryman,

2016). In addition, quantitative method would be significant for this

study to gather raw data and interpret those for demonstrating influence of

operating expenses on the income statement of CBA. In this context, annual

reports of the bank and official website of CBA would be major sources of data

that would help to gather statistical data. Now, as CBA is dealing with issues

of decreasing net profit margin, attempt to apply this deductive research

approach would help to collect information on the financial performance of the

company. It would also support to evaluate implications of net profit, gross

profit, expenses for technological adoptions while understanding the influence

of return on investment (ROI).

Since data points required for this

research is operational expenses and net profit after tax (NPAT), prime data

sources would be annual reports and official website of Commonwealth Bank of

Australia (CBA). Hence, keywords such as operating expenses , net

profit after tax , income statements and

income tax expenses would be used to track data points. This would be

effective to comment on effectiveness of financial performance of CBA while

understanding influence of operating expenses on profit margin. Based on the

selected method, data points and snips of data sources can be presented as

below-

Figure

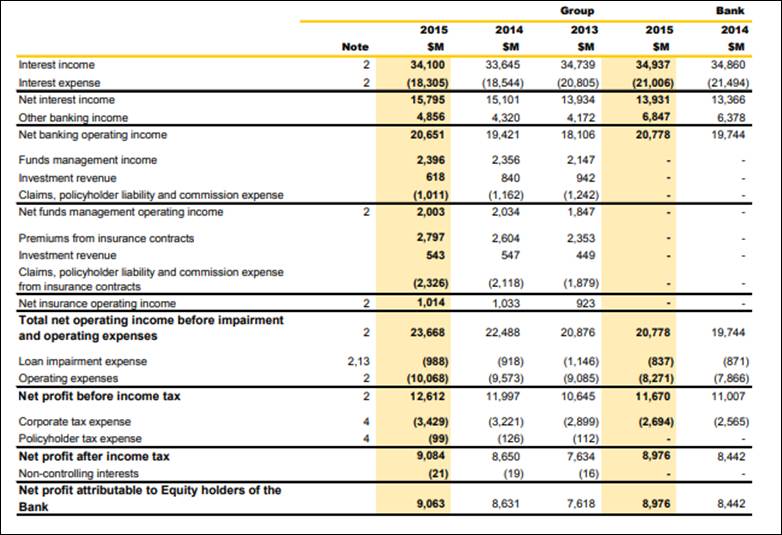

2: Income Statements 2015

(Source: Commbank.com.au, 2015)

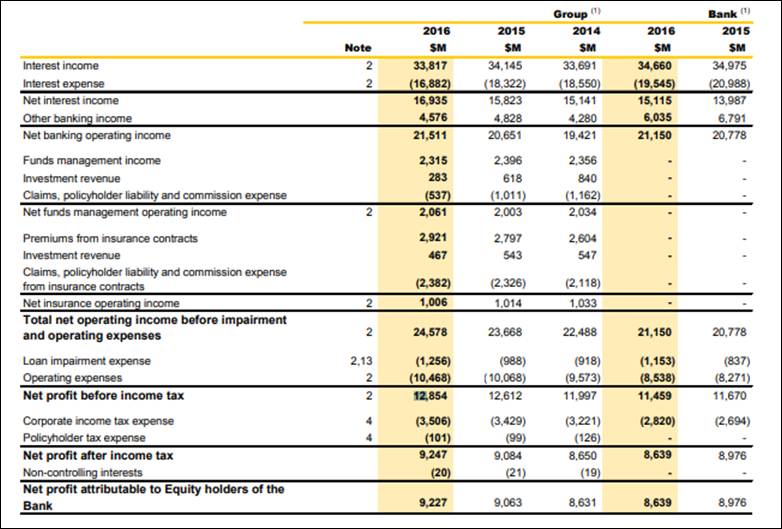

Figure

3: Income Statements 2016

(Source: Commbank.com.au, 2016)

Figure

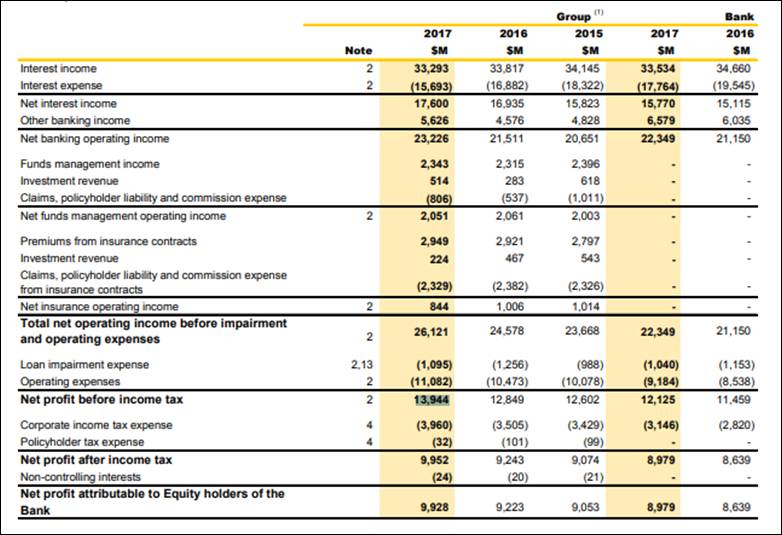

4: Income Statements 2017

(Source: Commbank.com.au, 2017)

Figure

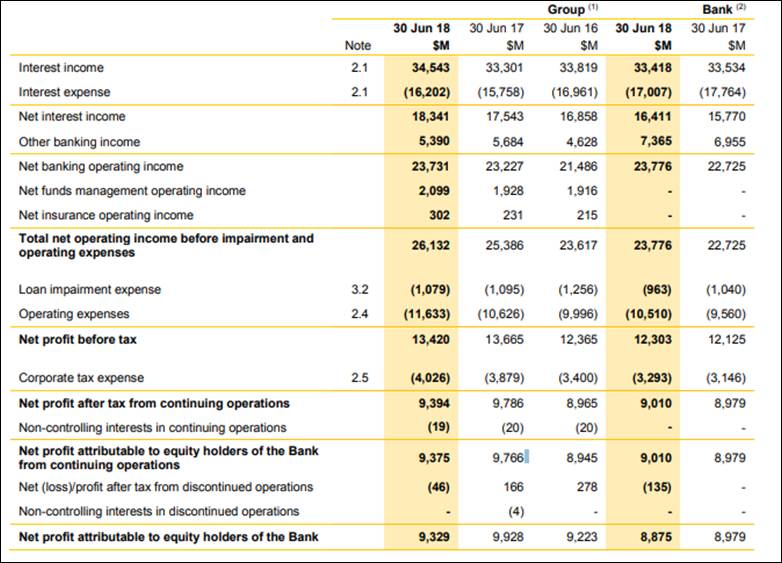

5: Income Statements 2018

(Source: Commbank.com.au, 2018)

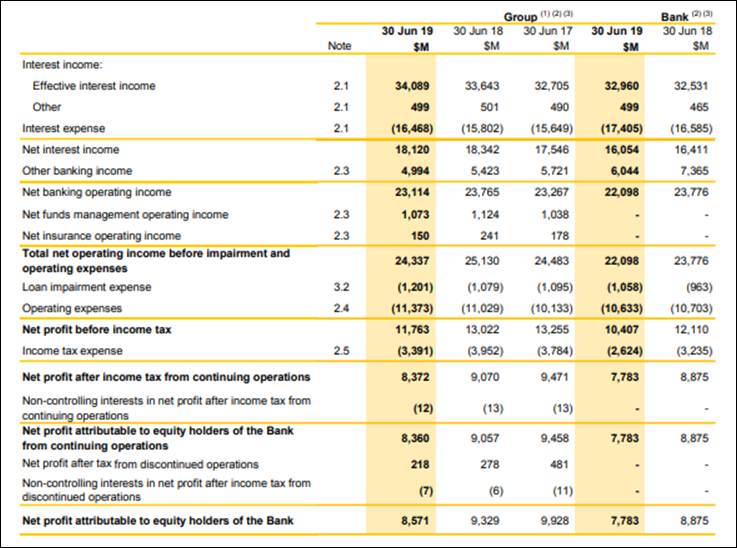

Figure

6: Income Statements 2019

(Source: Commbank.com.au, 2019)

Data

Collection Method and Technique of Data Analysis

Secondary method of data collection would be applied in this research to gather

statistical information on implication of operating costs on income statement

of CBA. In this regard, quantitative research method would

be selected to collect quantifiable information and conduct statistical

analysis for meeting research aim and objectives (Flick, 2015). Moreover, statistical information on

financial performance of CBA would be obtained from reliable sources including annual

reports of the company of the past five years ranging from 2015

to 2019. In this regard, official or commercial website of the company

would also be considered. Besides, suitable data points, in this context, would

be operating

expenses and NPAT (net profit after tax) of the

bank mentioned above. In addition, collected data would be evaluated using

analytical tools of Microsoft Excel and IBM SPSS. The former one would be used

to keep records of the data while the latter would help to interpret the raw

data and develop statistical tables and graphs.

Along with this, collected information would be

evaluated using relevant graphs and charts developed using the aforementioned

software tools. Furthermore, descriptive analysis, correlation

analysis, T-test and chi-square test would be performed

using IBM SPSS. These would help to explore the relationship between research

variables and test the hypothesis of this study to address research questions (Walliman, 2017). Focus on

evaluating secondary quantitative data collected from annual reports of past

five years of CBA would also be effective to comment on financial performance

of the bank. It would also support to identify efficacy of financial resource

allocation to identify potential areas of growth. Moreover, initiative to

statistically analyse collected data on operating expenses and net profit after

tax can present opportunity to comment on total income and expenses of the bank

mentioned above.

Research

Project Organisation

This research project would be

segmented into five different chapters that would contribute to the study for

identifying influence of operating costs on the income statement of CBA. The

chapters can be explained as following-

➢ Chapter 1: Introduction - This chapter will demonstrate the aim, objectives and

hypothesis of the study while providing a brief description of research

background and problem statement. It will also provide information on company

background and research deliverables to carry out further study.

➢ Chapter 2: Literature Review - It will review and analyse existing literature for

identifying factors that can influence operating expenses and eventually

influence profit margin. It will also discuss relevant theories and concepts

for generating ideas on financial performance of Australian banks.

➢ Chapter 3: Research Methodology - This chapter will discuss appropriate method to

conduct the study. It would deliver knowledge on the process of data collection

and analysis to meet research aim and objectives.

➢ Chapter 4: Findings, Analysis and Discussion - It will provide evaluation of obtained data and

discuss the findings of the study.

➢ Chapter 5: Conclusion and Recommendations - This chapter will conclude the entire research and

link objectives of the study with research findings while proposing

recommendations to address research questions. Moreover, areas of further

research and limitation of current research will also be highlighted in this

chapter.

Budget

and Scheduling and Justification

In order to conduct this study,

following estimation of budget can be considered, although this is subject to

vary depending on research requirements-

|

Area of Investment |

Estimated Budget |

|

Literature review |

$2500 |

|

Research resources

and data |

$2500 |

|

Data analysis |

$3000 |

|

Total Budget |

$8000 |

Table

1: Budget of the Research Project

Since this study has focused on

identifying implications of operating costs of CBA on income statements through

assessing net profit after tax (NPAT), access to secondary sources for

conducting literature review would require approx

$2500 to collect information from books and scholarly journals. In addition, an

amount of $2500 would be needed to collect statistical information regarding

financial performance of CBA. In this regard, information would be collected

from online web portals of the company as well as news articles and annual

reports that may cause changes in estimated budget. As analysis of obtained

information would require $3000 as it would require software to develop graphs,

charts and data illustrations.

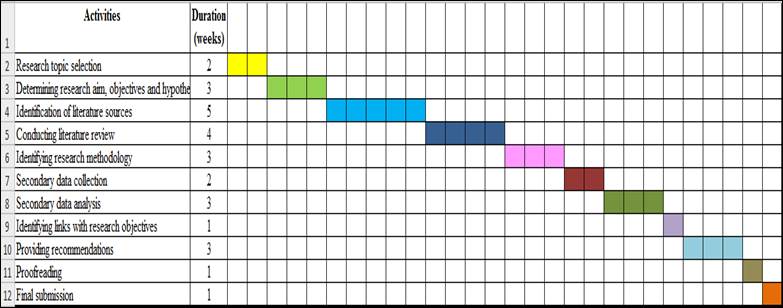

Gantt

chart

Figure

7: Research Schedule

References

Ahmed, A. D.,

& Ndayisaba, G. A. (2016). EFFECT OF CORPORATE GOVERNANCE ON CEO PAY - RISK

TAKING ASSOCIATION: EMPIRICAL EVIDENCE FROM AUSTRALIAN FINANCIAL INSTITUTIONS. The

Journal of Developing Areas, 50(4), 309-344. Retrieved from

https://search.proquest.com/docview/1844174959?accountid=188056

Alam, A. B. M.

M., Alam, M., & Hoque, A. (2019). SPENDING PRESSURE, REVENUE CAPACITY AND

FINANCIAL CONDITON IN MUNICIPAL ORGANIZATIONS: AN EMPIRICAL STUDY. The

Journal of Developing Areas, 53(1), 243-256. Retrieved from

https://search.proquest.com/docview/2094379135?accountid=188056

Bbc.com, (2018). Australia's Commonwealth Bank lost data of

20m accounts. Retrieved on 5th October 2019 from https://www.bbc.com/news/business-43985233

Bell,

E., Bryman, A., & Harley, B. (2018). Business research methods.

Oxford, UK: Oxford university press.

Bodle, K. A., Cybinski Patti, J., & Reza, M. (2016). Effect of IFRS

adoption on financial reporting quality. Accounting Research

Journal, 29(3), 292-312. doi:http://dx.doi.org/10.1108/ARJ-03-2014-0029

Borio,

C., Gambacorta, L., & Hofmann, B. (2017). The influence of monetary policy

on bank profitability. International Finance, 20(1),

48-63. Retrieved from DOI:10.1111/infi.12104

Bryman,

A. (2016). Social research methods. Oxford, United Kingdom: Oxford

university press.

Buckley, R.

P., Weber, R. H., & Dowell-Jones, M. (2015). A swiss

finish for australia? approaches to enhancing the

resilience of systemically important banks. Capital Markets Law

Journal, 10(1), 41-70. doi:http://dx.doi.org/10.1093/cmlj/kmu030

Commbank.com.au,

(2015). ANNUAL REPORT 2015. Retrieved

on 5th October 2019 from https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/cba-annual-report-30%20June-2015.pdf

Commbank.com.au,

(2016). ANNUAL REPORT 2016. Retrieved

on 5th October 2019 from

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/2016_Annual_Report_to_Shareholders_15_August_2016.pdf

Commbank.com.au,

(2017). Annual Report 2017. Retrieved

on 5th October 2019 from https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Commbank.com.au,

(2018). Annual Report 2018. Retrieved

on 5th October 2019 from

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/results/fy18/cba-annual-report-2018.pdf

Commbank.com.au,

(2019). 2019 Annual Report. Retrieved

on 5th October 2019 from

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/CBA-2019-Annual-Report.pdf

Commbank.com.au, (2019). Australia in 2019: Risks & Issues. Retrieved

on 5th October 2019 from https://www.commbank.com.au/content/dam/commbank-assets/business/industries/2019-03/risk-and-issues-2019.pdf

Daley, J.,

& Wood, D. (2016). Fiscal challenges for australia:

The next decade and beyond. Asia & the Pacific Policy

Studies, 3(3), 475-494. doi:http://dx.doi.org/10.1002/app5.146

Doran, M., &

Janda, M. (2018). Commonwealth Bank to

pay $700m fine for anti-money laundering, terror financing law breaches.

Retrieved on 5th October 2019 from https://www.abc.net.au/news/2018-06-04/commonwealth-bank-pay-$700-million-fine-money-laundering-breach/9831064

Flick,

U. (2015). Introducing research methodology: A beginner's guide to

doing a research project. Thousand Oaks, United States: Sage.

James, S.,

Sawyer, A., & Wallschutzky, I. (2015). Tax

simplification: A review of initiatives in australia,

new zealand and the united kingdom. EJournal of Tax Research, 13(1), 280-302.

Retrieved from https://search.proquest.com/docview/1784932060?accountid=188056

Jin,

K., Shan, Y., & Taylor, S. (2015). Matching between revenues and expenses

and the adoption of International Financial Reporting Standards. Pacific-Basin

Finance Journal, 35, 90-107. Retrieved from https://www.sciencedirect.com/science/article/pii/S0927538X14000870

Joubert, M.,

Garvie, L., & Parle, G. (2017). Implications of the new accounting standard

for leases AASB 16 (IFRS 16) with the inclusion of operating leases in the

balance sheet. The Journal of New Business Ideas & Trends, 15(2),

1-11. Retrieved from

https://search.proquest.com/docview/2002101028?accountid=188056

Kumar,

R. (2019). Research methodology: A step-by-step guide for beginners.

Thousand Oaks, United States: Sage Publications Limited.

Laing, G.,

& Dunbar, K. (2015). EVA(TM) EPS, ROA and ROE as measures of performance in

australian banks: A longitudinal study. Journal

of Applied Management Accounting Research, 13(1), 41-48. Retrieved

from https://search.proquest.com/docview/1694456692?accountid=188056

Newman, W., Mwandambira, N., Charity, M., & Ongayi,

W. (2018). LITERATURE REVIEW ON THE IMPACT OF TAX KNOWLEDGE ON TAX COMPLIANCE

AMONG SMALL MEDIUM ENTERPRISES IN A DEVELOPING COUNTRY. International

Journal of Entrepreneurship, 22(4), 1-15. Retrieved from

https://search.proquest.com/docview/2178087971?accountid=188056

Ogilvy, S.,

& Vail, M. (2018). Standards-compliant accounting valuations of ecosystems. Sustainability

Accounting, Management and Policy Journal, 9(2), 98-117. doi:http://dx.doi.org/10.1108/SAMPJ-07-2017-0073

Tang, Q.,

Chen, H., & Lin, Z. (2016). How to measure country-level financial

reporting quality? Journal of Financial Reporting and

Accounting, 14(2), 230-265. doi:http://dx.doi.org/10.1108/JFRA-09-2014-0073

Tran,

A. (2015). Can taxable income be estimated from financial reports of listed

companies in Australia. Austl. Tax F., 30, 569.

Retrieved from https://heinonline.org/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/austraxrum30§ion=26

Walliman, N.

(2017). Research methods: The basics. Abingdon, United Kingdom:

Routledge.

Wines, G.,

& Scarborough, H. (2015). Australian government budget balance numbers. Accounting

Research Journal, 28(2), 120-142. doi:http://dx.doi.org/10.1108/ARJ-01-2014-0001

Wong, K.,

& Joshi, M. (2015). The impact of lease capitalisation on financial

statements and key ratios: Evidence from australia. Australasian

Accounting Business & Finance Journal, 9(3), 27-44. Retrieved from

https://search.proquest.com/docview/1770070695?accountid=188056

Xu, W.,

Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements:

Operating to capitalised leases. Pacific Accounting Review, 29(1),

34-54. doi:http://dx.doi.org/10.1108/PAR-01-2016-0003

Yapa, P. W.

S., Kraal, D., & Joshi, M. (2015). The adoption of 'international

accounting standard (IAS) 12 income taxes': Convergence or divergence with

local accounting standards in selected ASEAN countries? Australasian

Accounting Business & Finance Journal, 9(1), 3-24. Retrieved from

https://search.proquest.com/docview/1678722109?accountid=188056

Yen, H. B.,

Sarath, D., & Ahmed, A. D. (2016). Efficiency of australian

superannuation funds: A comparative assessment. Journal of Economic

Studies, 43(6), 1022-1038. doi:http://dx.doi.org/10.1108/JES-05-2015-0088

Yeut,

H. T., Sultana, N., Singh, H., & Taplin, R. (2019). Busy boards and

earnings management an australian perspective. Asian

Review of Accounting, 27(3), 464-486. doi:http://dx.doi.org/10.1108/ARA-08-2018-0149

Zeller, T.,

Kostolansky, J., & Bozoudis, M. (2019). An

IFRS-based taxonomy of financial ratios. Accounting Research

Journal, 32(1), 20-35. doi:http://dx.doi.org/10.1108/ARJ-10-2017-0167

Appendices

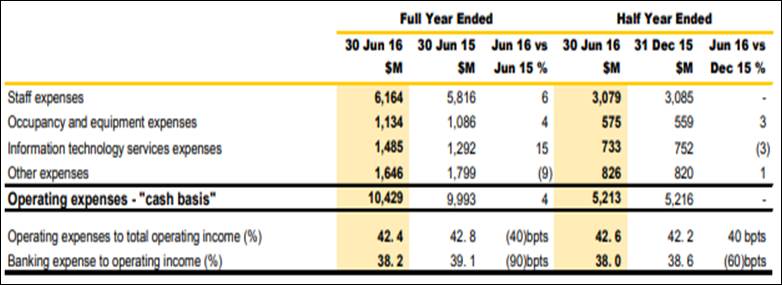

Appendix 1: Operating Expenses of CBA in 2016

(Source:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/2016_Annual_Report_to_Shareholders_15_August_2016.pdf)

Appendix 2: Household Debt (% of GDP)

(Source:

https://www.commbank.com.au/content/dam/commbank-assets/business/industries/2019-03/risk-and-issues-2019.pdf)

Appendix 3: Five Year Financial Report of CBA (from 2015 to 2019)

(Source:

https://www.commbank.com.au/content/dam/commbank-assets/about-us/2019-09/cba-annual-report-2019-spreads.pdf)