: 543

: 543

MEASURING AND EVALUATING THE CASUAL RELATIONSHIP BETWEEN CORPORATE

SOCIAL RESPONSIBILITY AND CORPORATE FINANCE

ACKNOWLEDGMENT

This d project is dedicated to my parents, who believed I could pursue

this dream, and to my wife and especially my son P, all have been a great

support during the whole journey of this course and especially this

dissertation. I am truly thankful for having all of you in my life.

ABSTRACT

After the

Doctoral Project is complete, the candidate wrote an abstract that summarizes

the study's purpose, the primary theoretical and conceptual perspective(s)

used, the major ideas developed in the study, and the implications of these

ideas. In order to conform to APA requirements, the abstract should not exceed

250 words. In a well-written abstract, a

reader finds the argument expressed clearly, as well as a statement about the

methodological approach. Although the

candidate writes the abstract after the completion of the study, the abstract

is placed at the beginning of the D Project.

Contents

1. CHAPTER

ONE: OVERVIEW OF THE STUDY

1.6

Theoretical and Conceptual Framework

1.12

Organization and Remaining Chapters

2. CHAPTER

TWO: LITERATURE REVIEW

2.3 The

theoretical basis of CSR

2.4 Critical

Evaluation of theories of CFP.

2.5 Critical

analysis of factors affecting CSR

2.5.1

External factors affecting CSR..

2.5.2

Internal factors affecting CSR..

2.6 Critical

analysis of the benefits of CSR

2.6.1

Impacts on company reputation.

2.6.2

Impacts on shareholders of the company

2.6.3 Impact

on employees of the company

2.6.4 Impact

of CSR on company management

2.6.5 Impact

of CSR on the environment

2.7 Critical

analysis of the factors affecting CFP

2.7.1 Effect

of financial factors on CFP

2.7.2

Effects of non-financial factors on CFP

2.8 Critical

evaluation of the impacts of CFP

2.8.1 Effect

of CFP on the stakeholders

2.8.2 Effect

of CFP on the employees

2.8.3 Effect

of CFP on the Consumers

2.9 Critical

evaluation of the relation between CSR and CFP

2.10

Illustration of the strategies to establish good CSR practice

2.11

Critical evaluation of the methods to establish better CFP

2.12 The gap

in the literature

LIST OF TABLES

LIST OF

FIGURES

Figure 2.1 Conceptual framework

Figure2.2 Carroll's CSR pyramid

Figure 2.3: Factors affecting CSR

Figure 2.5: Factors affecting CFP

Figure 2.7: Relationship between CSR and CFP

Figure 2.8: Strategies to establish good CSR practice

1. CHAPTER

ONE: OVERVIEW OF THE STUDY

1.1 Overview of

the study

Corporate Social

Responsibility has emerged as a factor that influences the financial

performance of an organization (Chuang & Tai, 2014). The present study aims

to:

(a) Provide

the responsibility between CSR and CFP so as to provide importance in relation

to the corporate social responsibility in Dell toward its internal and external

stakeholders and

(b) Determine

its impact on the financial performance of Dell during a given time period.

This study identifies the critical factors of CSR in case of Dell and

determines the importance of these factors in framing the relationship between

Corporate Social Responsibility (CSR) and Corporate Financial Performance

(CFP).

Investors and corporations show an increasing interest

in Corporate Social Responsibility (CSR), as it renders sustainable development

(Chuang & Tai, 2014). Regardless of the underlying uncertainty as to how

CSR affects the financial performance of a firm. As a result, many researchers

have explored the causal relationship between CSR and financial performance,

although they have achieved conflicting results. There is little evidence

showing that CSR and corporate financial performance (CFP) relate positively or

directly. The causal relationship between CSR as well as CFP is based on the

strategies about the usage of Dell in order to meet the social responsibility.

The relationship between the CSR as CFP is based on the factors on either

non-linear or based on the methods used in the non-existent case. The

non-linear relationship is proposed on the increment of the principle of CSR as

the theory is implemented in stakeholder's analysis. This study aims to

establish a causal relationship between the CSR and CFP as well as to measure

and evaluate this relationship. The company chosen for this study is Dell, a

multinational computer technology company based in Texas (USA). Specifically,

CSR effort, taken up by the company was be analyzed and evaluated to determine

the impact on the financial performance of the company.

1.2 Background of the Study

Fomukong (2014) stated that every

business aims to create wealth for their owners by offering products and

services that meet the market demand. However, in recent years, the focus has

shifted from mere financial gains to social responsibilities of the business.

For this study, CSR refers to the actions taken to do some social good, going

beyond the interest of the company as required by law (Sprinkle & Maines,

2010).

The issues related to the methods of implementation of

CSR activities is related to the eco-efficiency of the Dell, the engagement in

relation to the enhancement of the performance of the shareholders to improve

the working condition of the employee. The focus is altered from the financial

gains to the methods implemented in social gains to earn a high level of profit

related to Dell. The environment is to be managed in such a way that the

information technology related company earns a substantial level of profit in

business structure. The working condition of the employee who is working in the

organization associated with Dell must be improved to enhance the level of

productivity which resulted in a competitive advantage over other markets. When

the concepts in relation to CSR have practiced the operational increase in

sales, as well as the profit, is noticed along with an increase in quality and

efficiency.

As stated by (Peloza & Shang, 2011), the CSR

practices, as well as the achievement based on CFP, is interlinked with each

other as they aim to earn a sustainable amount of profit in the long-term

business scenario. The policy which is implemented in case of CSR activities is

interrelated as both these theories are achieved as a business model. On the

other hand, the principle about CFP is related to the purpose of enhancement of

the figures related to sales as well as to enhancement leading to productivity.

The CSR practices vary from country to country, so multinational companies have

to acquire knowledge about the country in which it operates (Chuang & Tai,

2014). Therefore, a multinational organization typically adopts a general CSR

approach that can be applied to the different units of the company in different

countries. As businesses develop a complex relationship with the communities in

which they operate, the direct impact of the business varies from country to

country (Jamali, 2016).

A comprehensive and multidimensional program for CSR

has three major parts: governance, social media, and the environment (Peloza &

Shang, 2011). Within each specific category, there are initiatives of CSR. This

study evaluated these initiatives and determined their impact on the financial

performance of the company.

This is a major threat which can be implemented for

the management of the specified Dell Company to identify, quantify, and unlock

the business value of CSR practices, thereby allowing business to allocate its

resources effectively. The business process helps to implement the CSR

approaches in relation to the performance by evaluating the economic,

environmental as well as the social factors. The profit of the dell is to be

enhanced to provide motivation of the employees as they are inclined to work in

a more balanced way. The profit scale has to be enhanced to increase the level

of sustainability as to implement better performance of the business firm.

1.3 Problem Statement

The measurement and evaluation of the causal

relationship between CFP and CSR change constantly; therefore, it is necessary

to conduct an up-to-date study that underlines the current phenomenon.

According to Brammer et al. (2012), previous scholars of this topic have

achieved varying results. Hence, the problem is that the current causal

relationship that exists between the CSR and CFP is unknown, as is the impact

of CSR practices on the CFP of the company in five years. The interrelation in

between the CSR as well as the CFP is vague study as the different implication

of the methods is not properly evaluated. The three aspirations in relation to

the performance of CSR vision is not properly evaluated as the team leaders did

not follow the rules and regulation appropriately.

1.4 Purpose of the Study

In this study, I propose to measure and evaluate the

causal relationship between CSR programs and CFP. Moreover, I seek to determine

if the implementation of CSR programs causes an increase in long-term sales and

gross margins. Financial performance has been defined in the context of

traditional accounting and measures, which are primarily market-based measures.

Some intervening variables, such as the size, growth, risk, preceding year

performance, and management preference have been controlled statistically in

this report. As commented by (Ghelli, 2013), the

size, growth related to the methods which were used in case of CSR activities

as they are involved in improvement related to the environment structure. The

process of CSR involved different types of finance which is essential for the

maintenance of valuable information on the investors.

This research investigated the potential impact of

Corporate Social Responsibility on the corporate financial performance of the

company. A full picture of the subject was being created by taking from the

previous theoretical research and examining results from previous studies.

Previous researchers have reached inconclusive results regarding the

relationship between CSR and financial performance (Ghelli,

2013). There is little evidence that CSR

and financial performance are related directly. However, companies devote their

resources, money, and efforts toward CSR activities, implying that there are

certain financial benefits for the companies to gain.

Thus, the purpose of this research is to fill the gap

in existing research and to render both the investors and the companies a

better understanding of the CSR efforts. Additionally, this study showed how

CSR efforts add value to the financial performance of the company. The results

which are obtained are useful as well as valuable for investors, the company,

and stakeholders, as they are involved, derive benefit from the CSR activities

of the company. In order to enhance the profitability in case of CSR activities,

the gap of the existing research is to be minimized to maintain long-run

profitability in case of the business organization.

1.5 Methodology

The methodology adopted for this study is a

mixed-methods research design. The company's initiatives during the period of

five years were be analyzed qualitatively, while the financial performance

shall be analyzed quantitatively by measuring the various financial ratios and

then determining the increase in sales and gross profit margin over a period of

five years. The financial performance of the company is to be analyzed in an

appropriate manner to improve the financial sustainability in case of cash flow

statement. The methodology aims to provide significance on the matter

implemented on enhancement used in the process of CSR.

1.6 Theoretical and Conceptual Framework

The business environment which was based on the

strategies which have resulted in enhancement of globalization as well as an

increase in the process of competition within the business organization, in

turn, helps to increase productivity. The business environment has become

challenging in today's era which is beneficial to improve the benefit related

to the stakeholders. The reputation of the business organization can also be

enhanced by adopting socially responsible activities. As stated by Adeleke (2014),

the firm presents their financial principle by CSR activities in their annual

report which has been presented in case of raw materials.

The stakeholder theory which is based on stakeholders

is crucial as it helps to maintain the business structure within the firm as

the theory is based on harmonization with the stakeholders. The stakeholder

theory is important as it helps to maintain the effect of key variables which

affects the financial performance of the company. The theory used six different

methods of the qualitative method which is used to analyze the profitability of

the firm.

The appropriate relationship between the different

employees of the firm results in improvement in productivity. The other methods

are products which are readily available in the market, the community which is

based on diversity of the employees. The methods used in governance are used

for utilization of environment to be implemented appropriately. The advantages

of the stakeholder's theory are that it takes into account the gross profit

margin as well as the total sales which are used for maintenance of economic

performance of the company (Orlitzky, 2013).

As commented by Weber (2008), the stakeholder's theory

is beneficial as the relationship in between the social as well as the

environmental performance of the company is maintained which depicts an inverse

shaped curved. The theory is chosen in the study as it helps in providing

analysis in maintaining the relationship in between the activities based on the

CSR activities as well as success in terms of economic value.

As opined by Orlitzky

(2013), the stakeholder theory is chosen as it was assumed the performance of

the employees in terms of economic values which is considered to be a dependent

variable. This theory is based on the importance of stakeholder which is

beneficial as it helps to produce such goods as well as the services which are environmental friendly in nature as well as which is

demanded by the customer. The theory also takes into consideration the nature

of the technology which is being used in the acquisition of raw materials which

results in enhancement of the scale of profitability within the firm. The

stakeholder's theory is chosen as it helps in evaluation of intensity within

the firm to increase the level of sustainability. The theory is used in this

study as it helps to maintain the pressure from the stakeholders to manage the

rules as well as the regulation of the firm. The rules and the regulation are

to be based in such a way that it helps to maintain the environmental

friendly behavior.

As opined by Orlitzky

(2013), the theory is chosen in this study as it consisted of both the internal

as well as the external stakeholders. The internal stakeholders comprise of

employees, the owners as well as the manager who are linked directly to the

company and are solely responsible for maintaining the image of the company in

its long term. The external stakeholders in case of stakeholder theory are the

suppliers, the government rules and the regulation on which the company

activities are dependent and the creditors.

As opined by Soana (2011), the customers and the

shareholders are responsible for maintaining the profit scale of the company.

The stakeholder s theory is important as it helps to maintain the relationship

in between the business enterprise as well as its internal and external

shareholders.

Thus, the stakeholder's theory is undertaken in the

study as it helps to provide strategy in maintaining the relation of the

company along with its stakeholders effectively and efficiently.

1.7 Significance of the Study

This study has many implications for executives, key

decision-makers, and owners of the business and the beneficiaries of CSR

activities (e.g., consumers, community, environment, stakeholders, and employees).

This study builds a foundation for future research. According to Soana (2011),

there has been an increase in the expenditures for CSR for which the chief

executive must decide how many resources were being allocated to make it

beneficial. Hence, this study is significant for such decision making, as it

provides information about the impact of the CSR activities on the financial

performance. The Dell Company may use the results of this study's implications

regarding contributions to its socially and environmentally-responsible goals.

1.8 Assumptions

It is assumed that the CSR practices being followed by

the company are comparable to industry standards and are easily available to

all the stakeholders. The next assumption is that all components of the CSR

initiative pertain to the CFP measures taken for the study. The most important

assumption is that the socially- and environmentally-responsible activities are

commensurate with the cultural practices of the country in which the company

operates, as the company has offices around the world.

1.9 Limitations

Several factors limit the outcomes of the study.

First, this study focuses on one computer manufacturing company; hence, the

results are unique to the company and are not generalizable for the whole

industry. The second limitation is that only a few variables will be considered

to determine the causal relationship between the CSR and CFP. The omitted

variables may affect the accuracy of the results. The limitation of the

research is that although the research is based on Dell assumptions have

already been taken that the CSR and CFP interrelationship is more relevant in

case of IT companies. However, the results obtained in the research may not

apply to other sector or other IT companies. This is because the research is

solely focused on factors affecting Dell not all IT companies in case of CFP

and CSR. In addition, it can also be seen that not all the factors applied in

case of Dell is applicable for the ethical and CSR index of other companies.

The third limitation is that the data for quantitative analysis is collected

for only five years; however, the company practices CSR activities and has done

so since its inception. In addition, regression analysis of the impact of the

variables of CSR such as the greenhouse emission and the renewable energy use

and the energy consumption with that of the CFP is also analyzed. This is done

based on the last five years report of CFP. The compounding effect of the CSR

activities was not taken into account, as it is seen from previous studies that

CSR activities do not generate results immediately. The fourth limitation is

that the data used in the study is secondary data and they have been generated

for a different purpose from which the implications for the study have been

derived. The secondary research has been used to establish the views of

previous research regarding the relationship between CSR and CFP and link it to

the existing regression analysis data of Dell. The secondary research although

was given a brief overview and was a help to establish the quantitative research.

However, the data from the previous research papers may suffer from lack of

reliability and validity. The fifth limitation is that accuracy and credibility

of the secondary data cannot be guaranteed.

1.10 Delimitations

The study is limited to the company itself, and only

two dimensions of the CFP are considered. The agenda of this research is to

examine and analyze the causal relationship between CSR and CFP in the chosen

company, Dell. The CSR variable is a multidimensional, ethical rating at the

individual component level. One way to measure CSR is the use of

multidimensional and ethical ratings. However, an alternative way was generated

by the researcher for the measurement of the CSR, which focuses on the perceptions

of the stakeholders. The primary data was collected by means questionnaires

from the stakeholders or by conducting an in-depth interview or as an

information disclosure that was related to the social conduct or was given as a

uni-dimensional social measure like, the reputation

of the company, environmental footprint, expenditure done on charitable

purposes or investment made for socially responsible activities. The

delimitation of the study is that the study clearly establishes the relation of

CFP with CSR and does not establish any relation with the operation and

production value of the company. It is not generalized and is very much

inclined to IT companies especially Dell. The study is confined only to the

analysis of the relationship between CSR and CFP and not in establishing the

relationship with other factors such as the employment relation and employee

turnover or the leadership practices. These factors although may affect the CSR

and CFP but are not considered in eth study.

1.11 Definition of Key Terms

External stakeholders: according to Orlitzky (2013), these are the groups of organizations or

people that are impacted by the firm or have an impact on the firm like

government, suppliers, customers, community, and trade unions.

Internal stakeholders: according to Orlitzky (2013), there are the sub-groups or the people

within the firm that can directly or indirectly influence the production and

the policies of the organization.

Management

discretion/preference: Soana (2011) stated that these are decisions related to the

spending by firms, which are entirely discretionary in nature.

Corporate governance: the means by which

any company is operated, controlled and managed to keep in focus the benefits

of the stakeholders, as defined by OECD (2008).

Environmental conduct: the behavior of the

business entity and how it treats the environment is an important resource in a

way that is sustainable and causes minimum or least harm as was proposed by

Idemudia, (2011).

As opined by Orlitzky,

(2013), the environmental conduct helps to maintain the behavior with respect

to the enhancement of the business organization which results in increasing the

sustainability. The enhancement in sustainability helps to achieve the required

treatment which was provided in case of the environment.

The main aim or objective of the business unit is

concerned with the business structure is to use the resources of the

environment in such way that it can be recycled and reused. The structure of

the environment is to be properly evaluated to maintain the sustainability so

that the resources which are non-renewable in nature are saved for the use of

future.

Environment footprint: The harmful or

adverse effects on society and the environment by the operations of the

business for which the corporations have social and environmental obligations

to reduce it to a level which is safe for the entire community.

Ethical conduct: The ethical consideration

of the business organization is used when the stakeholders undertake the true

as well as the fair value in case of preparation of financial terms. The

financial terms are to be prepared in accordance with the rules as well as the

regulation which is used in the enhancement of the profitability of the

organization. The main purpose of ethical consideration in case of business

enterprise is to maintain the confidentiality during the recording of data. The

internal control is also maintained within the organization to possess smooth

functioning in case of ethical consideration.

Financial reporting: Soana (2011) proposed

that these are the rules that govern the maintenance of the company s records

used in the preparation of the financial statements to be used by the

stakeholders of the company.

Greenwashing: As commented by Sun &

Cui (2014), the term greenwashing' is usually a practice which is based on

claiming the environmental benefits which are based on the products as well as

the final goods and services. This process as used by the company helps to be

more reliable in case of maintaining the products which are based on environmental friendly.

As opined by Soana (2011), the methods undertaken by

the company on the basis of greenwashing use the cost reduction method by

making the competitor more environmentally friendly. The process of green

manufacturing in case of changing the packaging system of finished goods as

well as on the method used in recycling process is beneficial.

Ozone layer: a layer in the atmosphere of

the earth; ozone depletion causes adverse effects on the plants and animals.

The ozone layer contains a high amount of ozone (O3) which is found in the

lower part of the stratosphere from about 20 to 30 kilometer above Earth.

Risk

management: the practice of identifying business risks, analyzing these risks

for comprehending them, assessing them to give them priority, and addressing

them by taking appropriate strategic actions. Risk management also implies

monitoring them for ensuring that remain within the limits of tolerance and

control, as given by Sprinkle and Maines (2010).

Social conduct: The concern of the

business firms for the working conditions of its workers and the living

conditions of all its stakeholders.

Social responsibility: It is defined as

the role of the business firm in supporting and improving society while

simultaneously pursuing the legitimate purposes of the business, profit and

shareholders wealth maximization.

Stakeholders: It is defined them as those

parties who are impacted by the operations of the firms and those who can

potentially influence the behavior of the firm.

Stakeholder theory: This theory states

that in the long-term, it is advantageous for firms to keep their stakeholders

happy with the operations of the firm.

As opined by Sprinkle and Maines (2010), the

stakeholder theory is based on improving the performance on the basis of both

the internal as well as the external stakeholders.

Sustainability: As commented by Sprinkle and Maines (2010),

the term sustainability' signifies the usage of the resources in such a way

the needs of the present generation are met without compromising the proper usage

in case of the future generation. The practice which is based on the economic

values, as well as the method implemented in social responsibility, is used in

case of protection done on the basis of environmental factors.

1.12 Organization and

Remaining Chapters

This doctoral project is well organized into five

chapters. The first chapters consist of introduction where the problem

statement, the purpose of the study along with the nature of study, definitions

and research questions are mentioned. The attempts were being made towards

measuring and evaluating a casual relationship

between corporate social responsibility and corporate finance. Chapter two

includes literature review which consists of the background information about

the research. The full range of theory related to the corporate social

responsibility, corporate finance, and relationship between the two was being

depicted. Chapter three was include the research methodology where the information on

the research design, number of participants and instrumentation used for

collecting data was be identified. This chapter also consisted of data

collection process, assumptions, limitations, delimitation and also the ethical

considerations related to the project. Chapter four consisted of the analysis

of the data collected. The data analysis

was being made and the conclusion was being drawn. Chapter five was follow the evaluation of the data collected followed by a

list of recommendations that are required to be followed for the purpose of

attaining high-end gains and profits from the corporate finance and corporate

social responsibility.

2. CHAPTER

TWO: LITERATURE REVIEW

2.1 Introduction

The current chapter on literature review takes into

account the theoretical basis of the Corporate Social Responsibility (CSR) and

the critical analysis of the factors affecting it. It also takes into

consideration the evaluation of the theories in regards to CFP and the critical

analysis of the factors affecting it. It takes into consideration the critical

evaluation of the impact of CSR on the company's financial statement as well as

the benefit of the stakeholders of using CSR. Apart from that, it evaluates the

impacts of CFP on the employees as well as the stakeholders. The dissertation

assesses the relationship between CSR and CFP on the basis of critical

evaluation. Lastly, it provides the strategies to implement a good CSR practice

as well as the gap in the present literature review.

2.2 Conceptual framework

Figure 2.1 Conceptual framework

Less cash flow is slowing down the

purchasing power Small size is giving less opportunity

to engage more staff Less cash flow in the economy

affecting CFP Size of the company affecting CSR The relationship between CSR and CFP The small size of the company is slowing down the CSR Stakeholders are losing interest in

investment

(Source-created by author)

2.3 The

theoretical basis of CSR

As commented by Wang et al. (2015), the Carroll's CSR pyramid signifies the

strategies of the organization to meet the social responsibility as it can be

accomplished by using four stages. The four stages can be the economic, legal,

ethical as well as philanthropic which can be followed by the business

enterprise to ensure that the business complies with rules and regulation or

not. On the contrary Tang et al. (2015), rejected this and commented

that the four stages are not required for ensuring a well establish business

structure, among that the two stages legal and ethical are vital to comply

rules and regulation. The legal structure takes into account the different

types of rules as well as a regulation which is essential for the maintenance

of long-term business. The ethical structure comprises of the rules as well as

regulation based on which a business acts ethically, and the financial

statement in regards to CSR are prepared with following the true and fair view

of GAAP (Korschun, Bhattacharya & Swain, 2014).

As stated by Shaukat, Qiu & Trojanowski (2016),

the CSR is based on the evaluation of economic values in accomplishing the

organizational goals as well as objectives. The economic values are based on

the assessment of the profit motive of the business as profit is the ultimate

source for the achievement of the long-term objectives. The profitability is

the only one way to achieve the long-term benefit which applies to both the

small scale as well as the large scale industries.

However, Saeidi et al. (2015) argued

and commented that philanthropic stages in Carroll's CSR pyramid are essential

for the evaluation of the long-term business objectives apart from the ethical

as well as legal values. The responsibility of the philanthropic stages is to

provide a proper result to the society at the end of an accounting period. The

donation, grants received by the project is vital for the evaluation of the

long-term aims as well as to maintain the upward rising of the profit scale. It

takes into consideration the luxurious things as they focus on strategies for

the improvement of quality life of the employees to provide motivation.

Figure2.2 Carroll's CSR pyramid

(Source-

Flammer, 2015)

As commented by P rez & Bosque (2015), the theory

of strategic leadership signifies that the Chief Executive Officer (CEO) has

the direct impact on the evaluation of CSR as are involved in the implication

of strategic CSR rather in case of average companies. On the contrary Orlitzky et al.

(2017) argued that there is no direct relation between the strategic leadership

as well as the evaluation of the company s growth. The business enterprise

growth can be enhanced by following both the ethical as well as economic

responsibility in Carroll's model of CSR.

As opined by berseder et al. (2014), the key features

related to the implication of Carroll's model of CSR are the evaluation of the

profit scale which is the vital factor for the foundation of any type of

business enterprise. The enterprise both short-term, as well as long-term, is

based on the factors of earning a profit in its long-term business prospects.

On the other hand, Obeidat, Tarhini & Aqqad

(2016), opposed this and commented that the business enterprise must comply

with rules and regulation as per the strategic leadership theory. The

organization can earn a profit when the rules, as well as the regulation, are

compiled, and the business enterprise follows the ethical practices in

Carroll's theory which is based on CSR.

As stated by Saeidi et al. (2015), Carroll's theory is simple to use and understand

as it helps to establish an emphasis on the importance of the profit scale. The

process associated with CSR is more adjustable as the business related to the

stakeholder model helps to evaluate the ethical values. On the contrary

Shaukat, Qiu & Trojanowski (2016), rejected and commented that the

Carroll's CSR model is complex in nature as the profit scale and the evaluation

of the ethics is not easily determined. The interaction of the responsibility,

as well as the social issues, is not determined which is crucial for

maintenance of profit scale in case of business enterprise. The responsibility

is based on an evaluation of both the long-term as well as the short-term

objectives in the evaluation of the profit scale in case of business enterprise

(El Ghoul, Guedhami & Kim, 2017).

Although there is opposition, the four stages in case

of Carroll's CSR model are crucial for the determination of long-term profit

scale and by compliance with ethical values in business enterprise.

2.4 Critical Evaluation of theories of CFP

As commented by Kim, Song & Lee (2016), the

futures of management theory provides the implication

of the future orientation in regards to the achievement of the long-term goals

as well as objectives. It takes into consideration the different types of

theories as it can be applied in case of variables as well as the management

philosophy. On the other hand, Shaukat, Qiu & Trojanowski (2016), argued

and commented that to achieve the high level of profit scale in case of a

business enterprise, the short terms objectives are also vital apart from the

long-term aims as well as the objectives.

As opined by Ba os-Caballero, Garc a-Teruel & Mart nez-Solano

(2014), the business management of the present business trend is notably

adapting the theories of CFP for making the business more sustainable. The

management theory of CFP is helping the business to grow in different technical

ways. This management theory of CSR is remarkably transforming the trends of

the business as it is using the digital platforms for managing the finance. The

management theory is helping in expanding the ways for business development.

Various new development features are adding up to the management theory of CFP.

As for example, artificial intelligence and robotics mechanisms were added up

for the betterment of the CFP in the business management.

On the contrary Brammer, He & Mellahi

(2015), argued that the implementation of an algorithm in the finance has made

the finance management stronger than before. Besides that, the gig economy is

also helping in the development of the business that is providing to be

beneficial for the companies. The CFP also includes the environmental

orientation that is helping it to enhance the acceptability in the business

market. CFP is always upgraded to implement various new features in it thus

this is helping the business to achieve the competitive advantages in the

market. The innovative new feature that includes into CFP is helping the

business to create new ideas for making the finance of the business stronger.

As opined by Cheng, Ioannou & Serafeim (2014), CFP

is expanding the social innovations for the business that is helping the

society to become more developed. The changing techniques for CFP always

support the up-gradation of the business and make the company unique in context

to the other business companies. CFP always adopt new methods that are

providing the companies opportunity to grab more new features into the

business. These enhanced features of CFP theories are helping CFP to evolve the

changing patterns of business. This new feature providing theories are

engraving remarkable milestones to flourish the business.

On the contrary, Dhaliwal (2014) argued that the

circumstantial prudence for the business development and orientation is fully

dependent on the methods that have been adopted by the companies. The

traditional theories of CFP are helping the business to evolve in a certain way

that is providing the business a feature of creating a bridge between new and

old methods. The evolution of theories helped the business to create profound

knowledge in the finance management. Due to this enhanced feature providing methods

the adaptation of CFP is making the performance of the business better. The new

theories of CFP are also helpful in business growth assessment that helps the

business in taking decisions regarding the business growth.

As commented by Ditlev-Simonsen (2015), the

forecasting feature of the CFP is helpful in decision making that helps the

business to adapt the changing pattern according to the need of the business.

The occasional updates helped the business to mitigate the wrong decisions

taken previously for creating the better business environment. Though the

features provided by the CFP is creating positive impacts for enhancing the

financial performance of the business but there have certain risks for this

quick decision-making technique of CFP. Since the decisions are always taken in

short time span thus, they may become error-prone for the business. As for

example, the forecasting of business growth may give wrong results due to the

short period assessment. The management theories that have been incorporated

into the CFP may damage the business orientation as they are not well verified

for their suitability on the business.

On the contrary El Ghoul, Guedhami

& Kim (2017) argued that there are wide ranges of strategies in CFP for the

business development that was helped in reducing the business risks for the

company. Beside that as per the traditional management theories, CFP also

contains topical management theories that provide the business liberty of

finding flaws in the business. The periodic up gradation of the new theories

helps the company to become alert for the upcoming challenges. The theories

that have been constructed on the basis of the business circumstances are

providing wider views regarding the upcoming risks of the business. Thus this helped the companies to assess the risk level of

the challenge correctly, and they can be able to take precaution to stand up to

the challenge.

2.5 Critical analysis of factors affecting CSR

2.5.1

External factors affecting CSR

As stated by Rao & Tilt (2016), the companies in the financial

sectors give more priority to the social measures and the environmental

measures than the commercial sectors. The production companies need to give

more priority to the environmental measurement than the other companies.

Besides that, the companies need to give the same priority to the social

measures. The people and the companies engaged with the real estate enterprises

do not value the social measure and this is a vital factor that is affecting

the society. The transport companies are doing the same thing that the real

estate companies are doing. On the other hand, as per the comment of berseder et al. (2014), it has been observed that the

academic sectors are less interested in giving priority to the environmental

measurement. The public works department of the society and the health and

private sectors are also losing their interest in giving priority to the

measurement of the environment. However, it is a remarkable fact that the

public enterprises, the private organizations and the health and academic

organizations are taking more interest in social measurement. These sectors are

taking a deeper interest in the social measurement.

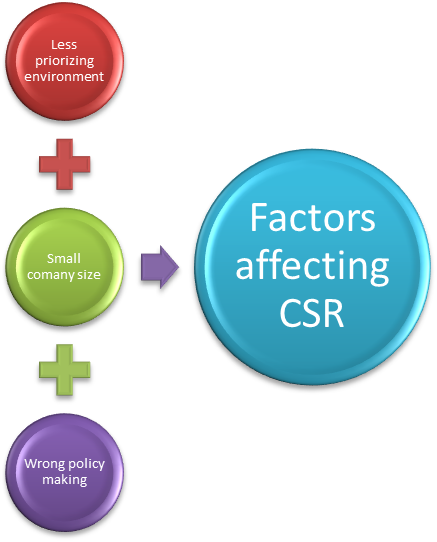

On the contrary Brammer, He &Mellahi

(2015) argued that many factors are affecting CSR but the first factor that is

affecting CSR is the company size. The size of the company is affecting the

social and the environmental measure in a very positive manner. As per the

research of Orlitzky et al. (2014), it can be

observed that the more the number of employees in a company, the better was the

effect on the CSR and thus the companies need to recruit a number of employees

that made the CSR stronger. Companies those are lagging behind for the less number of employees cannot take an important part

in the social and environmental initiative. Besides that, it is also a fact

that the small enterprises do not take an interest in the social and the

environmental measures due to their lack of financing capability in the

business. P rez & Bosque (2015) commented that the industries with huge

turnover always take an interest in the social, environmental measures due to

their huge cash flows in the business. Though the industries with huge revenue

take an interest in the social measures to make the business more profitable

and sustainable but they never show interest in the environmental measures.

As

opined by Cheng, Ioannou & Serafeim (2014), the main reason behind the

social measurement of the huge industries is that they are getting benefits for

the measurement. On the other hand, the environmental measurement is not

providing such a huge benefit for the companies. Thus

they are not showing any interest in this part of CSR. The companies are not

bounded by any barrier to take the environmental or the social measure. Due to

this reason, the companies are not having any legal issues regarding the

measurements. Besides that, the social and the environmental measure do not

have any effect on the market penetration of the companies. This is another

fact that is affecting the CSR, and thus the companies need to take a step for

the betterment of the environmental measurement. As opined by Obeidat, Tarhini & Aqqad (2016), though most of the companies do

not bother about the effects on CSR, few companies do this for the society and

customer satisfaction. In order to maintain the prospect of the company, all

the companies need to think about the impacts on CSR.

On the

contrary, Dhaliwal et al. (2014) argued that the cash flow in the business has

a significant effect on the CSR as it provides the company's ability to make

decisions. The cash flow in the business provides the ability to the companies

to take decisions independently. Higher the flow of the cash inside the

business, higher was the sustainability of the business. In this way, the

company made better revenue, and thus they can take rigid steps for the

betterment of the CSR. Thus the cash flow is another

factor that is affecting the CSR. Supported this as viewed by Lu et al. (2014),

the activities of the companies are also playing a vital role in the

development of CSR. In order to make more prospects the companies need to

implement specific rules and regulations for the well-being of the company. On

the other hand, increasing membership in the companies gives the companies

opportunity of getting various opinions. This helps the companies in taking

decision for the well-being of the company as well as for the wellbeing of the

CSR.

Figure

2.3: Factors affecting CSR

(Source: Malik,

2015)

As commented by Ditlev-Simonsen (2015),

companies need to form different bodies that can mitigate the problems

regarding the effects on CSR. In order to form these groups companies need to

engage people of different race. The companies need to promote the CSR in a

serious manner to mitigate the problems. The companies need huge funds for

promoting CSR and due to this reason; they have to think about the wellbeing of

CSR.

2.5.2

Internal factors affecting CSR

As commented by Kr ger (2015), this key role of the

financial companies can make the situation better for the CSR. The management

of the companies never focuses on the internal factors that are affecting CSR.

The wrong policies taken by the company is making the business more profitable

is also affecting the CSR growth. Thus companies need

to make stricter and more innovative policies and statements regarding the CSR.

Besides that, the internal roles of the employees of a company are also playing

a vital role in CSR.

On

the contrary El Ghoul, Guedhami & Kim (2017),

argued that the perceptions regarding the CSR are also a fact that is

internally affecting the CSR. The human resource management needs to take

decisions for making the CSR better. The governing body is not making rigid

steps for the CSR and due to this reason companies are not bothering about the

proper execution of CSR. Due to this, the companies are not giving proper

knowledge to their employees regarding the CSR which is greatly affecting the

CSR. Thus it is the duty of the companies as well its

employees to maintain proper CSR through effective understanding collaboration

between each-other.

2.6 Critical analysis of the benefits of CSR

2.6.1 Impacts

on company reputation

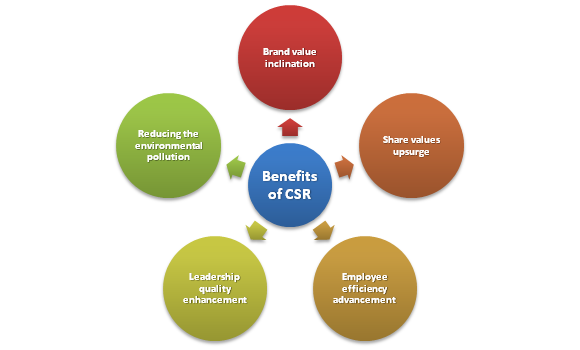

As commented by Flammer (2015), CSR has a great

contribution to the business as it provides many facilities and advantages to

the companies. CSR has no bindings of providing the features regarding the size

of the company. CSR increases the brand value of the products of the company as

it promotes the products inside the society. Beside that CSR also helps in

distinguishing the products and the qualities of the products distinctly.

Company reputation is a vital thing for the companies. Thus

the companies need to create a good reputation in the market. As stated by

Ditlev-Simonsen (2015) to improve the reputation of the company CSR plays an

important role. The corporate investments, as well as the investments for the

society, make the business company's image better to the mass of the society. Thus CSR can give the companies a competitive advantage and

to achieve the competitive advantage in the business companies need to make

small favors to their clients and the suppliers.

On the contrary Kang et al. (2015) argued that to make

the reputation of the company better inside the market the companies need to

behave well with the clients and the suppliers. This helped the companies in

achieving better position inside the market thus they were able to drag the

business in the global corridor.

2.6.2 Impacts

on shareholders of the company

As opined by Kim, Song & Lee (2016), the adaptation of CSR is

helpful for the company shareholders as it enhances the growth of the company.

The value of shareholders accelerates with the implementation of CSR in the company

and due to this reason; the shareholders of the companies grab more benefits

from the companies. The performance of the companies also upsurges with the

implementation of CSR in the companies thus the stakeholders grab a greater

percentage of benefits due to growth in the revenue. Besides that, the CSR is a

cost saving method and due to this, the company benefits increases.

This increment in the company revenue is added up to the shareholder's benefit.

On the

contrary, Korschun, Bhattacharya & Swain (2014)

argued that CSR increases the sale of the company thus the share value of the

company accordingly boosted up. This increment in the share value helps the

shareholders to increase their reputation. Beside that CSR helps in improving

the organizational growth thus the growth of the company helps the shareholders

to get more profit from the company. The most important benefit of implementing

the CSR inside the business is that helps in accessing the company capital.

Thus, this enhanced accessibility helps the shareholders to take decisions

liberally for the financial growth of the company.

2.6.3 Impact

on employees of the company

As commented by Flammer (2015), CSR helps the company employees in

personal skill development. The dedication of the organization can be increased

by implementing CSR in the business. In this way, the relationship among the

company employees can be enhanced that makes the performance of the employees

better. The CSR helps the company to find out the efficiency of the employee

and due to this feature, the employees get motivated in doing more work for the

wellbeing of the company. Besides that CSR is helpful

in developing the cooperative behaviors among the employees that make the

performance of the business better.

On the

contrary, Jenter & Kanaan (2015) argued that CSR helps in enhancing the

recognition of the staffs of the company. The social responsibilities of the

staffs can be enrooted within the staffs using CSR. This helps the employees to

become the socially responsible person and thus both the organization and the

employees get benefitted. Besides that CSR helps in

enhancement of employee retention that makes them more valuable employees for

the company. This enhanced commitment of the employees helps them to become

trustworthy for the company. Implementation of CSR is also beneficial for the

employees in making their prospects for the company. Thus

it can be seen that the employees work culture evolves due to the

implementation and as a result, the skills of the employees enhances.

2.6.4 Impact

of CSR on company management

As viewed by Kang et al. (2015), the incorporation of the CSR in the

company helps the company to attain more skilled management as CSR helps in

making skilled employees for the company. The betterment of the employee

performance was helpful in expanding the business thus the management

leadership was be appreciated. Lu et al.(2014),

supported this viewed that CSR also helps the company to expand the innovative

ideas regarding the business growth thus it was helped the management of the

company to implement new ideas for the wellbeing of the company. The

enhancement in the employee retention was helped the management to get more

trustworthy employees for the company thus the performance of the business

increased rapidly.

Figure 2.4: Benefits of CSR

(Source: Luo et

al. 2015)

On the

contrary, Kim, Song & Lee (2016) argued that the leadership quality of the

management can be enhanced using CSR in the business as it provides proper

training and knowledge regarding the business growth. Due to this reason, the

leaders became able to lead their subordinates in the right manner. The work

culture of the company can be improved using the CSR and due to this reason,

the commitment of the management for achieving global competitiveness also increased

accordingly. This helped the management in taking decisions liberally for the

company growth.

2.6.5 Impact

of CSR on the environment

As opined by Korschun, Bhattacharya &

Swain (2014), CSR has a wider impact on the environment as it helps the

business to develop moral values for the society. The implementation of CSR

helps in scaling down catastrophes that are harming the environment. CSR

provides knowledge to the company about the management of waste that helps to

progress the cleanliness of the society. Besides that, the waste management is

also helpful in recycling the wastes that help the companies in energy

management.

On the

contrary, Kr ger (2015) argued that CSR reduces the emissions of greenhouse

gases the companies that are beneficial for reducing the environmental

pollution. The knowledge of building eco-friendly offices helps the companies

to become socially responsible. The business risks can also be mitigated using

the environmental CSR and in this way, business reputation can be improved.

2.7 Critical analysis of the factors affecting

CFP

2.7.1 Effect

of financial factors on CFP

As opined by Lins, Servaes & Tamayo (2017), the CFP is eminently

dependent on the financial management. The enrichment of earning is directly

depending on the capability of earning a company. In order to make better

financial future the company needs to adopt different strategies that benefited

the financial performance. The nature of spending the money is another vital

factor that is affecting the CFP as less expense was make the business

opportunities narrow and spending too much can ruin the business.

On the contrary Luo et al.(2015)

argued that the investment in the business is also affecting the CFP as more

investment helped the company to take the decisions conveniently. Business

bodies need to store at least 10%-15% money for the security purpose that was

acting as the backbone of the business. Besides that

business administration needs to eliminate the unnecessary purchase of things

for the company. This unnecessary costing makes the CFP weak and as a result,

the performance of corporate funding scales down.

Figure 2.5: Factors affecting CFP

(Source: Post & Byron 2015)

As opined by Aguilera-Caracuel,

Guerrero-Villegas & Morales-Raya (2015), systematic tax payment makes a

business stronger. Thus companies need to pay taxes

periodically according to their earning. This lawfulness in tax payment makes

business more secure thus the sustainability of the CFP escalates. In order to

make the CFP progressive the investments need to be allocated to various

products of the company. This diversification in investment is a factor that

offers the CFP feasibility. Continual cash flow is a vital factor in making the

CFP viable and due to this reason companies need to make the cash flow steady

inside the business.

On

the contrary Friede, Busch & Bassen (2015) argued that the business returns

are playing a vital role in making CFP stable. In addition to this, the savings

for the growth of the business also needs to be verified periodically to make

the savings backbone for the future instabilities in the business. Beside that

rise in the non-performing assets of the companies creates an endangered

situation for the companies. Thus the financial

companies need to verify the customers before lending them to continue the

growth of CFP.

2.7.2 Effects

of non-financial factors on CFP

As stated by Haldar & Rahman (2016), there is a profound effect of

non-financial factors on the CFP. The first factor that influences the CFP most

is decision making. The companies need to organize meetings with the assistance

of administration on the laws and rules to evolve the CFP positively. The

present and the future steps creation for achieving the sustainability of the

CFP is an important factor. In addition, the policy-making of the company for

enhancement of the growth of CFP is a vital factor for the companies.

Hasan

et al. (2016) opposed this and argued that the industry needs to maintain a

good quality of the products to influence the growth of the CFP. Thus quality management of the company is a vital factor for

making the CFP growth stable. The companies need to focus on the standard of

the products that have been fixed by the standard maintenance board. Thus proper monitoring by the standard maintenance board is

a vital factor for the CFP growth of the company. The companies need to pay

attention to the employees' role towards the CFP sustainability achievement.

Employees are the pillars of the company thus their role is observed as an

influential factor in CFP growth.

As

opined by Ilhan-Nas, Koparan & Okan (2015),

employees' dedication to the work is another significant factor for proper

enhancement of the corporate performance. In addition to that employees'

understandability about the work and the work culture is a factor that helps in

improvement of the CFP. The employee retention procedure of the company is

observed as an integral factor for the CFP management. The role of the

relationship management of the company in maintaining the good relationship

between the customer and the company is also an effective factor that controls

the corporate financial performance directly. Thus the

administration needs to observe these relationship management policies very

carefully.

Simionescu

(2015) supported this and added that the business-friendly atmosphere of the

business locality is another vital factor that has a direct impact on the CFP

growth. As for example, the locality needs to have proper resource for the

development of the business. This was helpful for the CFP improvement of the

company and thus the company needs to choose right locality before

investment.

2.8 Critical evaluation of the impacts of CFP

2.8.1 Effect

of CFP on the stakeholders

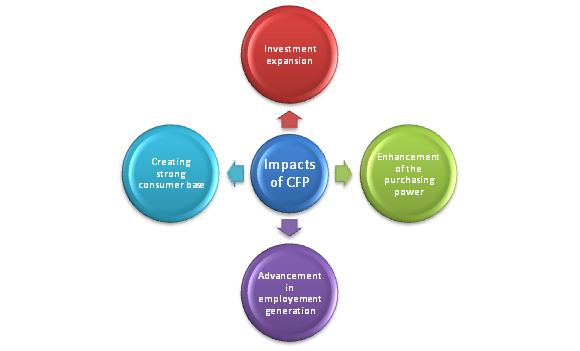

As stated by Isaksson & Woodside (2016), stakeholders are basically

categorized into two groups. The first group is categorized as internal

stakeholders and the second group is external stakeholders. CFP has a greater

impact on the internal stakeholders of the company as they are directly engaged

with the company. The employees and the management come under the internal

stakeholder's group. The performance of the corporate finance motivates or

de-motivates the stakeholders according to the progress of CFP. The financial

growth enhances the purchasing power of the company. Thus

the stakeholders become more liberal to purchase raw materials for the company.

On the other hand lack, Simionescu (2015) stated that

of purchasing power occur due to a deceleration in the CFP thus the

stakeholders become dependent on the other companies purchasing capability.

Hence companies need to maintain the growth of CFP to motivate the stakeholders

in seeking more investment for the company.

On

the contrary Javed, Rashid & Hussain (2016) argued that the external

stakeholders also get influenced by the corporate financial performance of the

company as they bear the key role in the business investment. The lack of

growth in the CFP prohibits the desires of investment of the stakeholders with

respect to investment in the company. In addition to this, the stakeholders

start searching for other growing corporate financial sectors for more profit.

Hence companies need to maintain stable growth in the CFP for seeking more

investment from the external stakeholders. The media partners are the external

stakeholders of the company. Due to this reason company needs to create

progressive CFP to influence the clients of the company with the media

assistance.

2.8.2 Effect

of CFP on the employees

As viewed by Lam et al. (2016), the size of the company employee is

directly proportional to the progress of CFP. The better progression in the CFP

attracts the number of employee and vice versa. Thus

CFP needs to have superior performance for the employment generation in the

company. CFP helps in the advancement of the salary structure of the employees,

and hence a larger number of people desire to get attached to the company. On

the other hand, Aguilera-Caracuel, Guerrero-Villegas

& Morales-Raya (2015) stated that financial recession makes the CFP weaker

and due to this reason the size of the company gets

reduced rapidly. Hence corporate financial performance needs to be upgraded to

the changing business requirements. Besides that CFP

also helps in employee motivation as employees before engaging with the company

search for the company revenue to get a better idea of the company. Thus employees

always desire to get engaged with the profit-making employers and CFP helps

them in getting proper knowledge about the company revenue.

Figure 2.6: Impacts of CFP

(Source: Rojas

et al. 2017)

On the contrary

Lin et al. (2017) argued that the cash management helps the employees to

release the stress. A healthy CFP provides employees extra motivation in

working more for the company well-being. An improved CFP helps in decision

making for the company, and due to this reason, the employees become efficient

in understanding the vision of the company. Hence the employees work

appropriately and progressively for the company's prosperity. In addition to

this better corporate financial performance supports the company's employee

requirements to create productive results for the company. In this way, the

employees become valuable employees for their employer.

2.8.3 Effect

of CFP on the Consumers

As stated by Linke & Jentoft (2016), CFP of the company works as an

indicator of the company growth for the consumers. CFP provides information

regarding the financial performance of the company that helps the consumers to

choose the right place for investment. In addition to this CFP is working as a financial

advisor to the consumers as unhealthy CFP indicates the deteriorating revenue

of the company, and thereby consumers become aware before investment. Besides that CFP helps in understanding the vision of the company

regarding their financial growth. The financial policies of a company for their

consumers can be easily identified with the assistance of CFP. CFP is helpful

for the consumers in determining the company honesty regarding the business,

and thus consumers can choose the right place for investment.

On the

contrary, Lucas & Noordewier (2016) argued that

CFP makes the companies conscious about the consumer interest. This benefits

the consumers as the companies try to rectify their errors to take more

competitive advantage of the market. On the other hand

not meeting the interest of the consumers makes the business weaker and in this

way, CFP becomes weaker. Due to this reason stability of CFP influences the

consumers in a very profound way. CFP is also advantageous for the consumers as

it increases the ease of doing social works for the society. Healthy CFP helps

the companies to do better service for the society and in this way society gets enriched with the help of CFP.

2.9 Critical evaluation of the relation between

CSR and CFP

As opined by Miroshnychenko, Barontini & Testa

(2017), CSR and the CFP are interdependent and indispensable to each other. In

addition to this, the governance of the company plays a major role in making

the relationship better between CFP and CSR. In order to understand the

relationship between CSR and CFP, the companies need to differentiate the

stakeholders' responsibility for the society and the company responsibility for

the society. The internal issues of a company must need to be distinguished

from the social issues to compose a better relationship between CFP and CSR.

On the

contrary, Muhammad (2015) argued that the administration of the company needs

to be focused on the relationship management among the stakeholders and the

society. Companies and industries manage the stakeholders' relationship with

the assistance of CSR, and the social responsibilities also judged on the basis

of CSR. Haldar & Rahman (2016) added that the policy-making of the company

is determined by the CSR whereas the CFP helps in deciding financial policies

for the company. CSR is also helpful in improving the reputation of the

company, and thus a large number of consumers can be attracted using CSR. On

the other hand, CFP helps the consumers to know the financial status and

financial performance of the company. Thus healthy CFP

also helps in enhancing the consumer base of the company by providing

information about the company financial health.

As opined by Ortas, lvarez & Garayar

(2015), CSR assists the companies in evaluating the responsibilities for the

environment, and the CFP status of the company helps the companies to decide

the required funding for the environmental benefit. The responsibility of the

employees for the betterment of the company is reflected by the CSR whereas the

CFP helps to determine the growth of the company. Thus

both the CSR and CFP evaluate the needs of the company for company growth.

Besides that, the CFP is determining the net profit of the company that

signifies the company growth and the CSR help the company to decide the amount

they can afford to contribute to the social development.

On

the contrary Park & Ghauri (2015) argued that CSR supports the company to

meet the consumer requirements and the CFP is helpful in accomplishing the

requirements for the consumers. The external stakeholders are also influenced

by CSR and CFP. CSR enhances the reputation of the company. Thus

it helps in seeking investment for the company according to CSR rating. On the

other hand, CFP reflects the financial strength of the company and due to this

better rating of CFP; it also plays a supportive role in bringing more

investment for the company.

Figure

2.7: Relationship between CSR and CFP

(Source:

Simionescu, 2015)

As viewed by

Rojas et al. (2017), the relationship of the CSR and the CFP is judged on the

basis of two theories that are good management and the stakeholder contract

cost. The good management theory supports the skill development of the

employees and the management using the CSR. In addition to this good management

theory also provides guidance on company strategy making. Wang et al. (2016)

supported this and stated that CSR helps the companies to measure the social

responsibility as well as the environmental responsibility. In addition, CFP

helps in money allocation for fulfilling the social and environmental

responsibilities. Besides that, the good rating in CSR indicates the positivity

in the business that attracts more investment of the company. Thus in this way, the revenue of the company becomes higher,

and due to this reason, the CFP also becomes healthier for the company.

On the

contrary, Wang & Berens (2015) argued that the reputations of the companies

can be enhanced using the CSR and thereby company size can be expanded by

engaging more number of employees. This expansion in

the company size helped the company to become productive, and thus the

financial stability of the company can be enhanced. This was help in developing

the CFP of the company. Hasan et al. (2016) supported this and stated that

companies try to achieve a good rating in CSR to motivate their employees as

well as making good reputation inside the market. This can be achieved by

giving proper training to their employees and meeting the employee demands.

Hence the reputation improvement offered the company more work-friendly

atmosphere. This work-friendly atmosphere, in turn, provided more efficient

workers that helped the company to compete at the global level. Thus the CFP rapidly increased due to the global

competitiveness of the company.

As opined by

Ilhan-Nas, Koparan & Okan (2015), the prosperity

in the CSR index of the company enables the company to mitigate the excess

expense for the company stakeholders. Thus the cost

management helped the company in enhancing the production. Due to this reason,

the CFP of the company accordingly increased, and the profit became higher than

before. In order to achieve this goal, the companies need to hear the

stakeholders' views regarding the company welfare. Thus

the stakeholders rely more on the company, and due to this reason, CSR rating

became much higher.

Opposing

this fact Isaksson & Woodside (2016) argued that, companies can take the

competitive advantage by mitigating the external and the internal challenges of

the company. Companies need to handle efficiently the problems between the

company management and the employees to make the company growth sustainable.

The cost transaction related problems need to be mitigated to create a good

reputation. The companies need to be engaged with different NGOs that helped

them in improving social and moral values. These factors helped the company to

improve their CSR and thus their brand value was an increase.

Javed, Rashid & Hussain (2016) supported this and

stated that improved consumer base would help the company to make a higher

profit and hence the CFP was also got increased. The companies need good

governance and need to have a broader view regarding the social and

environmental growth. Opportunistic attitudes may damage the reputation of the

company. This damage to the company reputation has reduced the stakeholders'

interest in investment in the company. Thus the CSR

was get damaged due to reputational damage and CFP was be harmed due to the

reduction in investment.

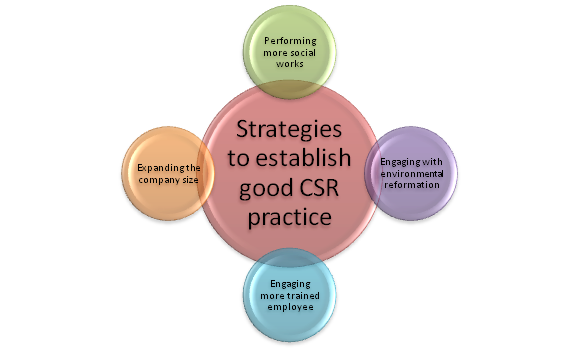

2.10 Illustration of the strategies to establish

good CSR practice

As viewed by Lam et al. (2016), in order to flourish the business in a

positive manner, the companies need to make strategies that helped them to

become socially responsible figures. Companies need to train the employees

about the social values and the way they are abided, for maintaining the social

responsibilities. The leaders of the companies need to establish by themselves

few examples regarding social responsibilities that was motivated the

subordinates to follow the leaders. Lin et al. (2017) supported this and added

that as for example the leaders of the company could organize few charity

programs for supporting the backward classes of the society. This made a

greater impact on the employees as well as in the society regarding the good

initiatives of the company. Hence company can get a large number of consumers

and the employees became socially responsible. Thus by

making this strategic reform inside the company both the company and the

society can become beneficial.

On the

contrary, Linke & Jentoft (2016) argued that the companies need to make

themselves environmentally responsible figures. Companies occasionally need to

host programs regarding the environmental welfare that helped the employees to

turn themselves into environmentally responsible people. This also made the

environment beneficial which in turn help the company to become eco-friendly.

Lucas & Noordewier (2016) supported this and

commented that the companies need to organize few programs that spread a good

message to the mass of the society regarding the environmental reformation.

Companies can host reforestation programs that helped in reducing the pollution

level. Reforestation also helped the company to reduce the greenhouse gas

effect in the environment. Hence this responsible attitude helped the company

to seek positive stakeholders' investment. Thus the

CSR result of the company can be enhanced in this way.

As

opined by Miroshnychenko, Barontini & Testa

(2017), companies need to enhance the size that helped them in penetrating the

market. The enhancement in the number of employees enabled the companies to

create a better quality of services for their clients. In this way, the

companies can make the service improvement and thus the acceptability of the

products also got boost up. Muhammad et al. (2015) supported this and stated

that the enhancement in the employee number would help the company to expand

the business in a sustainable manner. The well-developed size of the employees

made the company enable to become a global company by expanding the

productivity. Thus in this way the company can get the

opportunity to serve more number of people within the society. This increment

in the social service helped the company to improve the CSR level.

On

the contrary Ortas, lvarez & Garayar

(2015) argued that the improvement in the company size helped the company to

get engaged with more number of people from different

communities and cultures. Thus the mixture of

different communities and adaptation of various cultures helped the company to

transform themselves according to the demand of the society. Park & Ghauri

(2015) supported this and stated that the mixture of different community and

culture would help the companies to create a greater impact towards communal harmony

and this was beneficial for the society. Thus the CSR

of the company can be ascended and the people of the society relied more on the

ability of the company.

Figure

2.8: Strategies to establish good CSR practice

(Source:

Simionescu, 2015)

As opined by Aksak, Ferguson

& Duman (2016), in order to make the CSR rating better the companies need

to infuse various new products periodically. Infusion of these new products

helped the company to attract the number of customers and investors due to

their uniqueness in the market. Thus the brand value

of the company also scaled up. The new products need to be introduced in the

society with good quality maintenance. In order to infuse new products in the market companies need to have a steady cash flow and for

achieving this CFP of the company needs to be healthy.

Opposing this fact Andreu, Casado-D az & Mattila

(2015) opined that, to maintain the viability of the CSR the companies need to

realize the product demand inside the company. These concerns of the companies

convey their responsible attitude towards the society and thus the society was

be benefited. The responsible attitude of the company for the society helped

them to raise the customer base. Batty, Cuskelly &

Toohey (2016) supported this and stated that In order

to infuse new products into the market companies need to maintain the

environmental criteria. The new products of the company need to be introduced

into the market after checking their environment friendliness. Thus this helped the company to reduce the environmental

criteria as well as the business can be expanded in this way.

As viewed by

Chung et al. (2015), companies need to learn the talent management procedure to